Beyond Ionomers: Regulation Drives Demand for New Fuel Cell Membranes

As regulation continues to drive demand for New Fuel Cell Membranes, Hydrogen Industry Leaders examines the latest IDTechEx report into the Materials for PEM Fuel Cells outlook.

Membrane materials are of fundamental importance for fuel cells. So significant, in fact, that they typically give their name to the fuel cell, as is the case for Proton Exchange Membrane (PEM) fuel cells, with IDTechEx forecasting the market for ion-exchange membranes in PEM fuel cells to be worth over US$1.1 billion by 2033.

Typically, the material of choice for PEMs is an ionically conducting polymer known as an ionomer. These ionomers are one of a family of perfluoroalkyl substances (PFAS), and concerns are mounting regarding PFAS, with alternative materials beginning to emerge.

The new IDTechEx report, “Materials for PEM Fuel Cells 2023-2033“, gives a detailed technical overview of membranes and other key components for PEM fuel cells, an analysis of the major players, and also includes granular 10-year market forecasts for key fuel cell components and materials in terms of both units and volume. IDTechEx has also extensively covered the electric vehicle industry and forecasts demand for fuel cell electric vehicles (FCEVs) in “Fuel Cell Electric Vehicles 2022-2042“.

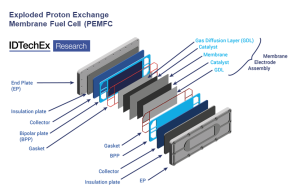

An exploded schematic of a PEM Fuel Cell, highlighting the central role played by the membrane. For further information on fuel cell membrane technology and other key fuel cell components, see the IDTechEx report “Materials for PEM Fuel Cells 2023-2033“. Source: IDTechEx

The PEM enables the functionality of the fuel cell by transporting protons from one side of the cell to the other while keeping the different fuels separated. In the report, IDTechEx provides extensive benchmarking of the market leader against competing ionomer materials for three of the most critical parameters for PEMs; electrical resistance, ion exchange capacity (IEC), and membrane thickness.

Despite transporting protons, it is imperative that the membrane has high electrical resistance to avoid short-circuiting the cell, while the combination of high IEC and thin membrane increases the fuel cell performance by enabling rapid proton transport. Promising alternatives exist, with performance exceeding the market leader in the three previously mentioned categories; however, the latter remains dominant due mainly to its position as the first mover in the market.

Tougher Regulations Will See The Reduction of PFASs

Although dominant, ionomers are a PFAS-containing material and are subject to many of the concerns relating to PFASs. PFASs are considered “forever chemicals” due to the strength of the fluorine-carbon bond, with several health risks associated with accumulation in the human body, such as liver damage, kidney cancer, and reduced response to vaccines.

PFASs are transferred to the water cycle during their manufacturing stages, use in industrial processes and end-of-life treatment, leading to inevitable exposure for organisms. Bioaccumulation occurs in the tissue of organisms, such as fish in polluted waters, and this is then transferred up the food chain, including to humans.

The manufacture and utilization of PFAS chemicals are becoming subject to increasingly tough regulations. The European Commission banned the use of PFASs in a number of areas, including fire-fighting foams in 2021, intending to limit their use to applications of critical societal importance, while the European Union may potentially restrict all uses of PFASs by 2025.

In December 2022, the US EPA issued an add-on memo to the National Pollutant Discharge Elimination System (NPDES) program aimed at accelerating efforts to reduce PFAS discharge to waterways.

The US are Already Working on Alternate Options

On the back of these current and proposed restrictions, many companies are moving to reduce their reliance on PFASs. An interesting case study is the American company 3M. Having produced PFASs since 1947, 3M announced in December 2022 that it will cease the manufacturing of, and work to discontinue the use of, PFASs by 2025.

3M cited regulatory restrictions, consumers becoming “increasingly interested in alternatives” and operational difficulties as primary reasons for exiting the PFAS market.

So, what does this mean for fuel cells? Ultimately IDTechEx expects to see the beginning of a transition away from PFAS membranes to alternatives (including hydrocarbons) within the next three to five years. Prototype developmental projects are underway with various OEMs and novel materials gaining traction, predominantly at an academic level, such as metal-organic frameworks (MOFs), although these materials are still at an early stage with little commercial uptake.

Historically, hydrocarbons have not seen success as membrane materials due to their tendency to disintegrate in the harsh chemical environments within the fuel cell. However, recent advances at companies such as Ionomr Innovations have seen the development of hydrocarbon ion-exchange membranes capable of fulfilling the requirements for PEM fuel cells without the health and environmental concerns associated with PFAS chemistry.

For more details on the materials demand, trends, and emerging novel alternatives to the incumbents for PEM fuel cells, please see the IDTechEx market report “Materials for PEM Fuel Cells 2023-2033“.